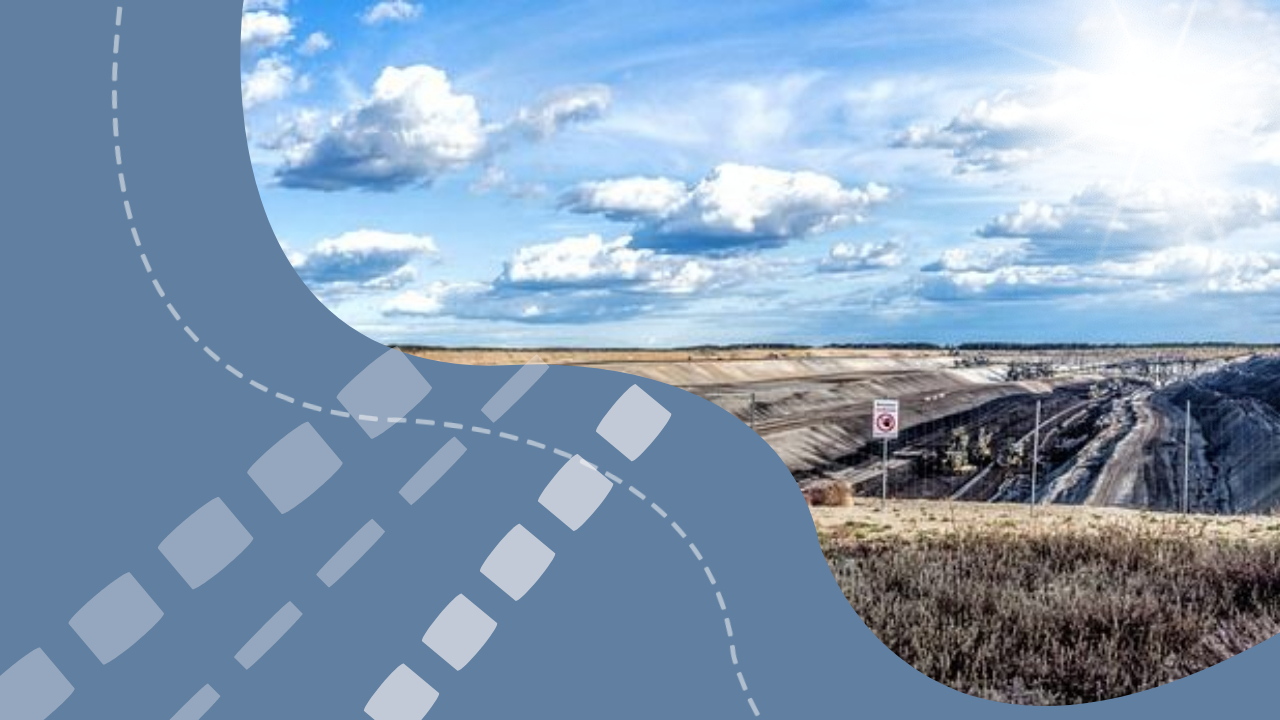

Ukraine has granted Turkish conglomerate Onur Group exclusive access to exploit some of its most prized mineral reserves—including graphite, kaolin, and gold—marking a significant step in international investment amid regional conflict and economic uncertainty. The company is expected to launch operations in 2026, starting with what may be Ukraine’s largest graphite deposit in the Khmelnytsky region.

According to reports from Czech outlet Body Guru, Onur Group currently holds five special mining permits. These include one gold deposit in the Dnipropetrovsk region, three kaolin sites spread across Kirovograd and Dnipropetrovsk, and the massive Gorodnyavskoye graphite deposit. The latter boasts 143 million tonnes of approved ore with an average graphite carbon content of 5.14%, promising up to 130 years of extraction potential.

The graphite project has been recognized by the European Union as strategically important, reinforcing its role in securing Europe’s supply of critical raw materials essential for electronics, electric vehicles, and green technologies.

Despite initial optimism, Onur Group has walked away from the gold deposit after discovering far lower-than-expected mineral grades—just 1.4 grams of gold per tonne, compared to the projected 4.5 grams. This economic mismatch rendered the project unfeasible.

While four of the five mining sites remain in preparation stages due to logistical and security challenges near conflict zones, Onur’s efforts represent more than just a commercial venture—they also illustrate Turkey’s strategic push to increase influence over key mineral supply chains.

As global competition intensifies over rare earth elements and industrial minerals, Ukraine’s openness to foreign investors may offer both risks and rewards. For some, the move raises concerns over sovereignty and long-term control of national resources. For others, it signals a pragmatic path toward economic recovery and integration with Western supply chains.